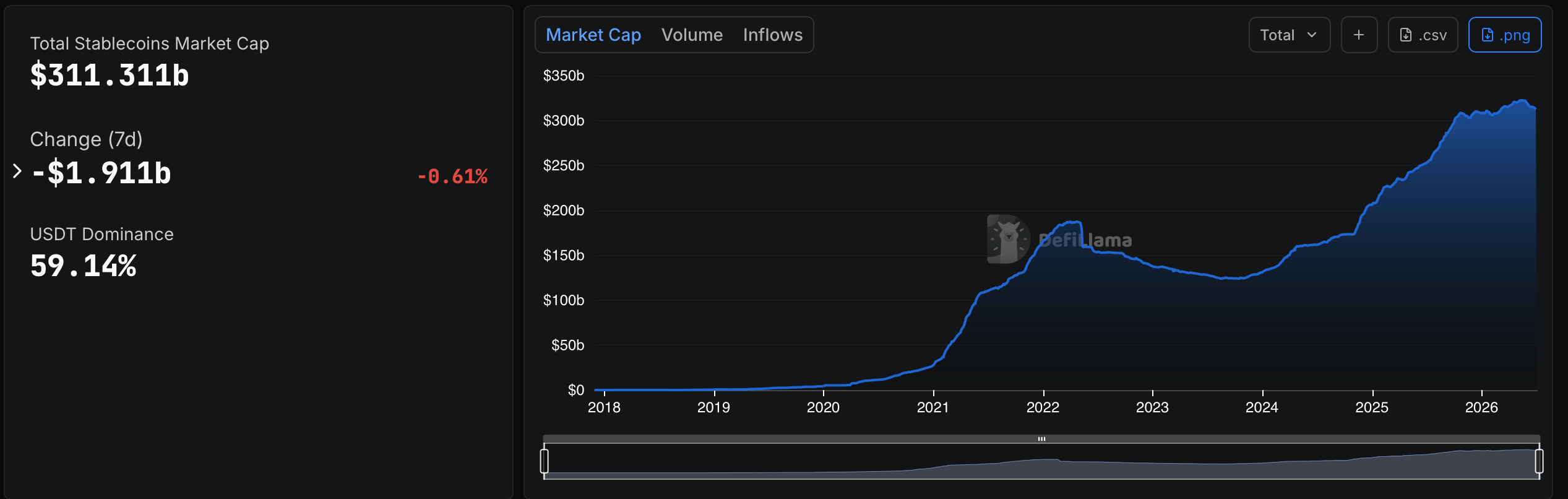

The total stablecoin market cap has declined by $10 billion since May 2026, falling to $290 billion. The sharpest drop occurred in June with $7.7 billion in outflows - the largest monthly decline since the Terra-Luna collapse in 2022. However, analysts emphasize this 3% correction remains far milder than 2022's 26% crash and reflects natural market consolidation after record growth.

%22%2F%3E%3Crect%20width%3D%221600%22%20height%3D%22900%22%20fill%3D%22url(%23a)%22%2F%3E%3Crect%20width%3D%221600%22%20height%3D%22900%22%20fill%3D%22url(%23b)%22%2F%3E%3Cpath%20d%3D%22M100%20720%20C380%20520%20470%20760%20740%20560%20S1180%20420%201500%20640%22%20fill%3D%22none%22%20stroke%3D%22%23fff%22%20stroke-width%3D%222%22%20opacity%3D%22.22%22%2F%3E%3Crect%20x%3D%22132%22%20y%3D%22122%22%20width%3D%221336%22%20height%3D%22656%22%20rx%3D%2256%22%20fill%3D%22%23fff%22%20fill-opacity%3D%22.08%22%20stroke%3D%22%23fff%22%20stroke-opacity%3D%22.22%22%2F%3E%3Ctext%20x%3D%22190%22%20y%3D%22238%22%20fill%3D%22%23a7f3d0%22%20font-family%3D%22Inter%2CArial%2Csans-serif%22%20font-size%3D%2234%22%20font-weight%3D%22800%22%20letter-spacing%3D%228%22%3EBDNEWS24.NET%3C%2Ftext%3E%3Ctext%20x%3D%22190%22%20y%3D%22350%22%20fill%3D%22%23fff%22%20font-family%3D%22Inter%2CArial%2Csans-serif%22%20font-size%3D%2262%22%20font-weight%3D%22900%22%3E%D0%9A%D0%B0%D0%BF%D0%B8%D1%82%D0%B0%D0%BB%D0%B8%D0%B7%D0%B0%D1%86%D0%B8%D1%8F%20%D1%81%D1%82%D0%B5%D0%B9%D0%B1%D0%BB%D0%BA%D0%BE%D0%B8%D0%BD%D0%BE%D0%B2%20%D1%83%D0%BF%D0%B0%D0%BB%D0%B0%20%D0%BD%D0%B0%20%2410%20%D0%BC%D0%BB%D1%80%D0%B4%20%D1%81%20%D0%BC%D0%B0%D1%8F%202026%20%D0%B3%D0%BE%D0%B4%D0%B0%3A%20%D0%BF%D1%80%D0%B8%D1%87%D0%B8%D0%BD%D1%8B%20%D0%B8%20%D0%BF%D1%80%D0%BE%D0%B3%D0%BD%D0%BE%D0%B7%D1%8B%3C%2Ftext%3E%3Ctext%20x%3D%22190%22%20y%3D%22720%22%20fill%3D%22%23cbd5e1%22%20font-family%3D%22Inter%2CArial%2Csans-serif%22%20font-size%3D%2230%22%20font-weight%3D%22700%22%3EIT%20%2F%20AI%20%2F%20Crypto%20%2F%20Security%3C%2Ftext%3E%3C%2Fsvg%3E)

Outflow Distribution Among Major Stablecoins

RWA.xyz data reveals uneven impacts across stablecoin issuers:

- USDT (Tether): $6 billion decline from $190B to $184B

- USDC (Circle): $7 billion drop from March's $80B peak

- USDG (Paxos): 12% growth to $3.2B driven by Robinhood integration

Three Key Drivers of the Decline

1. Post-Growth Correction

The stablecoin market doubled during 2024-2025 before hitting $300 billion in October 2025. Current contraction represents natural consolidation after this rapid expansion. Historically, such corrections last 3-6 months before resuming upward trends.

Additional pressure came from capital rotation into traditional assets following the Fed's rate hikes to 5.75%. Fidelity reports $4.2 billion moved from crypto funds to Treasury bonds in June 2026.

2. Cooling Crypto Market Activity

Bitcoin's consolidation between $60,000-$65,000 reduced demand for stablecoins as trading instruments. CoinMetrics data shows stablecoin trading volume dropped 22% month-over-month in June, with decentralized exchanges (DEXs) seeing 35% declines.

Margin trading constraints also emerged - platforms like Binance and OKX reduced USDT pair leverage from 10x to 5x, cutting monthly turnover by $1.8 billion.

3. Regulatory Shifts

The US GENIUS Act temporarily slowed stablecoin adoption by Visa and Mastercard as partner banks paused transactions for compliance audits. This particularly impacted USDC, whose payment volume fell $1.2 billion monthly.

Europe's MiCA framework now requires reserve transparency - forcing Tether to allocate an additional $800 million to liquid assets, temporarily reducing portfolio yields.

2022 Crash vs. 2026 Correction

| Metric | 2022 | 2026 |

|---|---|---|

| Decline Magnitude | 26% ($44B) | 3% ($10B) |

| Primary Causes | TerraUSD collapse, FTX/Celsius bankruptcies | Systemic correction, capital rotation |

| Recovery Timeline | 18 months | Projected 3-6 months |

Analyst Projections: 2026-2030

Despite short-term volatility, experts remain bullish:

- Citi: Base case $1.9 trillion by 2030

- Standard Chartered: $2 trillion by 2028

- Wincent: Growth of regulated stablecoins (USDG, USDGO)

Bernstein highlights stablecoins' B2B payment potential - potentially capturing 15% of cross-border transactions ($1.5 trillion) by 2027, especially in Asia and Middle East regulatory sandboxes.

Crypto Market Impacts

Reduced stablecoin liquidity has already:

- Increased BTC/ETH volatility by 15-20%

- Decreased DeFi activity (TVL down 8%)

- Shifted liquidity toward Bitcoin ETFs

Secondary effects include lower ETH staking yields (down from 5.2% to 4.1% APY) and 30% NFT price declines as speculative capital dries up.

Key Monitoring Points

- USDT/USDC recovery patterns

- SEC responses to new stablecoins post-GENIUS Act

- Chainalysis data on major exchange flows

Circle's upcoming reserve report will be pivotal - if Treasury holdings exceed 90%, it could boost institutional confidence.

Emerging Stablecoin Competitors

Despite market contraction, new entrants are gaining traction:

- OpenUSD: $500M raised by payment consortium

- EURG: Euro stablecoin by Commerzbank

- CNYG: First regulated yuan stablecoin (Hong Kong Monetary Authority)

Notably, Mitsubishi UFJ's hybrid XGD (50% yen/50% gold) begins testing in Q3 2026 with FSA oversight.

Investor Risk Factors

Current conditions require attention to:

- Potential fiat conversion delays from compliance checks

- Rising network fees (especially Ethereum) for large transfers

- Reserve differences: USDT (85% Treasuries) vs USDG (100% bank deposits)

Additional risk comes from proposed US Treasury rules - a 0.1% tax on stablecoin transactions over $10,000 could deter hedge fund participation.

Questions & Answers

Why is USDT losing market cap faster than USDC?

USDT dominates retail trading while USDC serves institutional needs. Reduced retail activity disproportionately impacts Tether. Some users also migrate to USDC for its regulatory compliance and transparency.

Which stablecoins are growing despite the downturn?

USDG (Paxos) and USDGO gained 12-15% through traditional finance partnerships. USDG's Robinhood integration and 0.5% yield offering particularly stand out.

How did Terra-Luna affect current conditions?

The 2022 algorithmic stablecoin collapse accelerated adoption of fully-backed models. Today 98% of stablecoins use fiat collateral. Stronger reserve requirements have improved sector stability.

Could shrinking liquidity crash Bitcoin?

Short-term volatility likely, but long-term BTC trends depend more on macroeconomic factors. JPMorgan notes current liquidity remains 40% above early 2025 levels.

Which regions show stablecoin adoption growth?

Southeast Asia saw 18% quarterly growth (Singapore, Thailand). Argentina led Latin America with 25% increases due to hyperinflation.

How have issuer reserves changed?

Recent reports show:

- Tether increased Treasury holdings from 58% to 85%

- Circle reduced corporate bonds from 20% to 8%

- Paxos now uses only bank deposits/reverse repos

Which banks support stablecoins?

Beyond Silvergate/Signature, 2026 saw:

- BNY Mellon (USDC settlements)

- Standard Chartered (USDG servicing)

- DBS Bank (CNYG pilot)